What should India's r* be?

What should India's r* be?

Thinking about this phantom, complex yet important economic/financial variable

“95 per cent of economics is common sense made complicated, and even for the remaining 5 per cent, the essential reasoning, if not all the technical details, can be explained in plain terms”

Ha-Joon Chang, South Korean "heterodox" economist, University of Cambridge

Economics, especially financial and macro-economics, can come across as rather intimidating. Part of it is the regular gatekeeping experts do, especially in academia, wanting to protect their turf and which happens in all walks of life. Part of it is that a lot of macro is still very much in flux aka even the experts sometimes do not always know what they are talking about or at the very least actively disagree with each other. Part of it is the pendulum swinging away from what used to be understood as political economy grounded in historical, path-dependent analysis towards the other extreme of statistics and stylised universalist modelling, signalling a strong underlying physics/math envy. Finally, it takes a lot of an effort to explain complex phenomena in simple but not simplistic terms.

Therefore in the spirit of Chang’s quote above, let me try to simplify one of the more esoteric concepts floating in economics: r* or the real natural/neutral rate, knowing fully well that I am likely to (at best) partially succeed in this somewhat-longer-than-an-oped piece. This is the inflation-adjusted rate of interest at which the economy is neither over-heating nor burdened with over-capacity.

The rate in question in turn is the (generally) short-term risk-free rate of the country in question, that is, the interest rate the government pays to borrow overnight or up to a few days/weeks (say) and the interest rate that the central bank sets. Generally speaking if there are more investment opportunities than savings, r* should be higher and vice versa. But of course for smaller/emerging economies, it is even more complex because often they are more likely to be “price takers” in terms of global cost of capital than say the United States, but there is always some policy or otherwise friction.

If inflation is say 4%, as is India’s target, and if r* is 1% then India’s risk free neutral rate in *nominal terms* should be 5%. That is the rate at which inflation should not increase nor should unemployment; hence another acronym often used - Non Accelerating Inflation Rate of Unemployment or NAIRU for the lowest possible unemployment rate which does not overheat the economy (it is not zero because there is always some re-skilling, switching of jobs etc.)

Continuing with this example - if you are higher than 5% in terms of the (say) reverse repo rate aka ‘rate at which the RBI borrows from banks’ that better be because of high inflation risking a price-wage spiral in a tight labour market, allowing enough subjectivity for some short term or cyclical factors of course. If we are below this (r* + inflation), it better be because of ‘output gaps’ in terms of lost ‘potential’ GDP or not enough employment (not just in terms of unemployment but also how many working age adults are looking for a job in the first place).

Interestingly enough, both the “high inflation” and “output gap” stories look prima facie true in post-pandemic-war India/world as of today. No easy quantitative answers (like what a Taylor or equivalent rule may spit out, as necessary as these frameworks are) - beware the math/physics envy once again. Next year we perhaps might be more focused on output gaps like this year we are on inflation.

But let us not worry about how would we use r* if we knew it. Let us first estimate what it is. Because it is a rate that is back-calculated and a rate that changes over time.

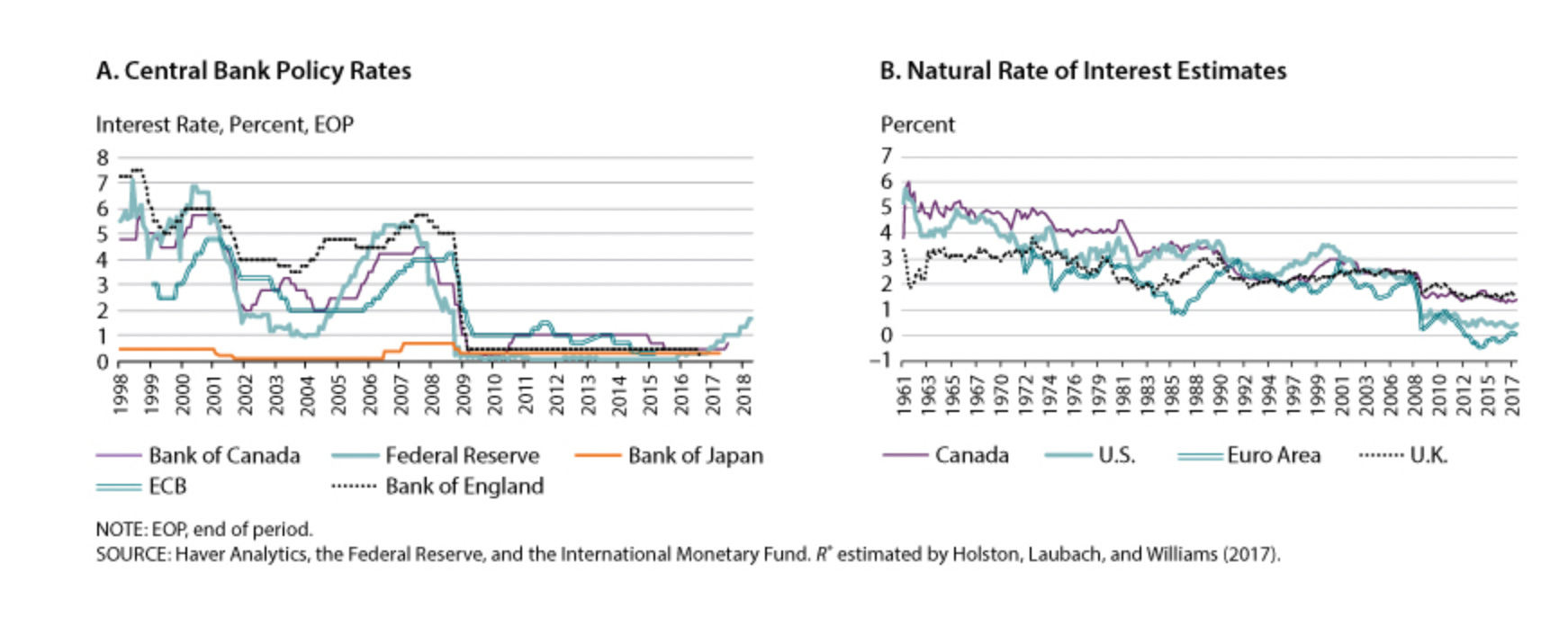

Let us first begin with the United States, the country with the deepest and most liquid markets of the world. Recently, the Fed Chair Powell hinted that at around 2.25-2.50% short term interest rate, the US had hit neutral aka the real rate is 0.5% or a bit less assuming the 2% inflation target over time still holds as the Fed claims it does, and which the market by and large still believes though the debate over the shorter term is much more contentious. (Technically, the Fed targets what is known as PCE and the TIPS market operates on the basis of CPI but I am again getting into the alphabet soup…)

More importantly, this near 0.5% real rate in the United States, if broadly true, has been falling for decades (image below via this.)

Some conservatively estimate one percentage point per decade fall over the last generation. In India too r* has been falling and is estimated at almost 1% today by some. In fact, emerging economies may have seen a faster falling in r* than developed ones albeit starting from an even bigger spread. None of these trends of course can blindly be linearly extrapolated and none of the snapshot numbers should be seen as any kind of precise truths. But more data and sharper analysis can help in better triangulation, or as Neelkanth Mishra (of Credit Suisse) calls his writings - “tessellatum” or a mosaic ‘piecing together disparate data for economic and market insights.’ One is also reminded of the nuanced Jain/Dharmic concept of Anekantavada but I digress.

Declining productivity growth rates and ageing societies are some of the factors behind this phenomena though it is important to emphasise that r* seems to have fallen much more than growth rates (as a very rough proxy of productivity; indeed in terms of per capita growth rates - the below graph from here may show an even bigger divergence.)

Now, India r* in a relatively open capital account situation should be equal to:

The US r* plus some risk/liquidity premium minus (and this is often forgotten) adjustment for the expected real appreciation of the rupee versus the dollar.

[Explanation: Emerging Market or EM assets are perceived to be riskier/shallower than Developed Markets or DMs generally although in the case of India/large EMs vs a few DMs, one can quibble but let that aside so that explains the premium. Secondly, if adjusted for inflation differences, a currency is likely to appreciate in relative terms as is likely to happen with a faster growing country over long periods of time, then to that limited extent the latter’s cost of capital should be lower.]

Say the premium is very roughly around 100 basis points (although this number is very volatile) and the appreciation is say 50 basis points (if one does a relative analysis of India’s and US’ broad REER on a through-cycle basis). In which case, India’s r* should be around 50 bps higher than America’s which is what the estimates linked above show (US ~30-50 bps, India ~80-100 bps). That means with an inflation target of 400 bps, India’s nominal neutral rate should be just short of 5% indeed. India’s repo is around there right now though the reverse repo is much lower (and currently inoperative), similarly America’s is also near its neutral nominal rate as mentioned above (but after diverging more in proportionate terms than India).

This shows that India’s central bankers as well as fiscal policy decisions over the last 2-3 years deserves praise, unlike 2017-18 when there was a clear over-tightening perhaps in response to “gain” credibility (in front of whom?) after demonetisation. Yet we cannot always rely on good central banking, and it is here that an ever more open capital account for a large/growing economy and friendly/neutral polity serves as a forcing function. Understanding where the r* of any country is going - at least intuitively - is critical for any global asset allocator (choosing countries, equity vs bond etc) as well as for any serious policy maker.

I will end this post by making three brief comments.

First, as inflation recedes in early 2023 and the base effect of lower Q1FY22 Indian growth is washed out by then, India’s lost potential output (compared to pre-pandemic trend) will become clearer prompting r falling below r* again. Secondly, over the long term while some are talking about a global inflation revival based on inequality and demographics (although that seems dubious given the example of Japan), for both factors the growth of India is underestimated. Global (as opposed to intra-country) inequality is on the margin falling because of the rise of India and while China is joining Europe and Japan in ageing, India still has a large labour force yet to be globally tapped (not just in goods, but in increasingly tradable services as well). Finally, a renewed focus on infrastructure/green technology/industrial-trade policy globally may perhaps gradually revive physical investment (over and above digital investments) leading to a stabilisation/mild increase of r* though there are big uncertainties here.