The Economist is wrong on India yet again

Growth in India 2020s will very likely surprise on the upside.

Apologies for not writing here for sometime.

I was busy with my day job (investing - where I am afraid many of us might confuse luck with skill if things don’t change - but things always change!), and with promoting my (coauthored) book “A New Idea of India” through various podcasts etc. I am very pleased to say that the book has received an excellent reception (into its third print, which is apparently not bad for an Indian hardcover nonfiction book). I am also very honoured to share that the Prime Minister of India read and liked the book.

I will try to write more frequently going forward. All feedback is welcome - I am sure I will be making a few errors here, as a substack unlike a column (or a book!) does not go through somebody else’s eyes first. Moreover, if I have to write more often here, it has to be somewhat stream-of-consciousness. Kindly excuse in advance.

All feedback is still welcome. You can tweet to me @HarshMadhusudan and follow updates about the book @ANewIdeaOfIndia

***

In their “world in 2021” series, The Economist (Tom Easton) writes that the Indian economy “was sick before the coronavirus crisis” and that “it will still be unwell when the pandemic has passed”.

Yes, “GDP growth has been declining since 2016, and investment since 2018” but that could very plausibly just signify a down business cycle (which is increasingly global and overlaps with a strong dollar phase) and many reforms taken by the Modi government which have clearly been about short term pain, long term gain - (1) bankruptcy code while enabling REITs, INVITs and the bond market (though more remains to be done (2) indirect tax harmonisation, (3) labour and agricultural reforms, (4) infrastructure investments, (5) inflation targeting (6) foreign currency reserves accumulation.

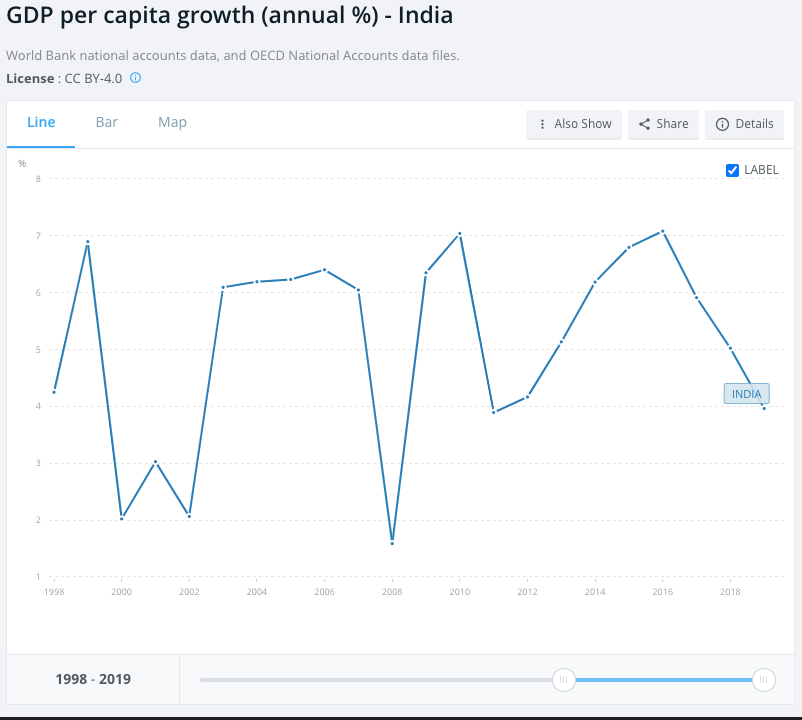

If instead of the above the government had done (1) “bad bank” + bank recapitalisation, (2) massive personal income tax rebates for the middle class, (3) huge agricultural minimum support price (MSP) plus minimum wage increases for formal labour, (4) gargantuan national level farm loan waivers (5) significant inflation adjusted interest rate cuts earlier (6) lower foreign currency reserves accumulation - then yes we could have had higher growth (in both rupee and dollar terms) and higher inflation since 2017 or so - just like we had from 2009 to 2012. Even so, the growth rates have not been very different as this chart (1998-2019, per capita real growth, India, World Bank) shows. [1998-2004, 2014-2019: BJP+ governments; 2004-2014: INC+ governments]

In any case, the BJP government chose quality and sustainable growth rate over a sugar high, and still won re-election with an increased majority. That is the stuff political economy dreams are made of. Clearly, that is too much nuance for The Economist which in both 2014 and 2019 wanted India to vote against Narendra Modi.

Now, there is nothing wrong with an economic sugar high once in a while - almost everybody needs a cheat weekend once every few months. The problem with being excessively Spartan, especially in a self righteous manner, is that beyond a point it can become a self fulfilling prophecy. And while it may still work for individuals, for economies it can be suicidal. Fortunately, we are not at that point yet and the pandemic has already made sure that story has stopped.

Personally, I think the economy could do with a real estate led sugar high for the next year or so - real estate is manufacturing that cannot be imported, and time bound massive tax incentives to buy real estate and to borrow for it are needed (including by the rich, sorry ‘upper middle class’). The government is partially coming around to that view, including at the states’ level somewhat.

However, the Indian political economy headline for the last 6-7 years must be that PM Narendra Modi has done huge aka ‘big bang’ reforms while preserving macro dry powder. While overdoing the latter, especially by the RBI perhaps, was a bit of a mistake that became increasingly discussed by 2018 or so, relative conservatism continued even in 2020 partially because of the border tensions with China.

Even so, we may still be not doing as much as needed and the Finance Minister has just hinted that the coming Budget will be more growth oriented. I have no doubt given India’s strong fundamentals - demographics, reforms, technology, density - India will do very well in the 2020s.

Then The Economist will be forced to keep using the word “exceptions” more and more as it does when it talks about Reliance gradually becoming a global tech player and Apple along with the rest of Silicon Valley investing in India. Only “Orientalist” descriptions of the “bookseller, phone repairman and chaiwallah” seem to give British expat journalists some solace in India. They just do not like when the latter - a chaiwallah - gets to run the country, a country they once ran. But I digress.

The basic issue remains simple: India’s deflator (rough average of CPI and WPI, and more stable than headline CPI) remains benign and most of our borrowing is in local currency at the sovereign level. While that was not as smart as some retired technocrats like to think, it nonetheless is more of a reason to now borrow extensively (especially in rupees and to a lesser extent in dollars, euros, yen) to invest in our defense indigenization, primary healthcare, secondary education and hard infrastructure.

I have earlier talked about the $1T, $3T and $5T framework for trade openness vs capital openness for a large but poor country like India. It is fine to open our capital account more, and have some mild protectionism for a few years as we go towards $5T. We may have to re-open towards trade after that but that does not mean that some activist trade/industrial policy is going back to “license raj” as some lazy commentators imply.

Since our currency is not overvalued in any absolute sense, we can and must spend more - so long as we do not waste it. Which means that the government must not give in to either public sector unions or so-called farmer unions who just represent the rich farmers (relative to the average Indian farmer.) Decent pensions for our soldiers is the right thing to do but geographically concentrating procurement of cereals and opposing farm reforms is not.

If we work harder on our governance - a lot remains to be done indeed - India will do even better. But even with current levels of governance, no one can stop the return of faster growth in India. At a $2,000 per capita base with improving state capacity, excellent demographics and with a world full of liquidity and innovation nothing - almost nothing, not even The Queen’s English - can stop India from becoming an economic superpower within a generation.