RBI has done an excellent job but it needs to better leverage Modi-Sitharaman's work

Fiscal restraint, structural reforms and infrastructure all need to be further leveraged by India's monetary policy.

As per the first advance estimates of FY24, India’s nominal GDP growth slowed to 9% from 16% in FY23. But real GDP growth for both years was similar at slightly more than 7%, an impressive number given global circumstances. Yet this shows that a massive deceleration in the deflator (a proxy for economy-wide inflation not just consumer-facing) from around 9% to less than 2%. Most of the change came from a fall in commodities- or goods-dominated wholesale price inflation. Now a near-8 percentage point fall in one year is no trifling matter.

With the inflation target (2 to 6%) being based on consumer-facing prices for the Reserve Bank of India (RBI)’s Monetary Policy Committee (MPC), this creates an uncomfortable situation. The rates have been on a hold for about a year at 6.5% (although they are effectively higher given recent liquidity deficit). When producer prices had surged globally, the RBI had raised rates by 250 basis points.

The CPI-based inflation meanwhile has broadly been in the same range for the last few years – near the upper end of the inflation target, and sometimes higher. So this shows the problems of asymmetry and arbitrariness, despite the current central bank leadership arguably being much more professional than its predecessors. Monetary policy is being kept tight when nominal growth is much lower than trend. This is part of a broader problem. Over the last decade, Indian consumer prices have increased by 5.1% compounded while the deflator has grown by 4.2%.

As the fiscal projections are made for FY25, a reduced nominal GDP growth will perhaps be taken (we will know on 1 Feb - say 10% or thereabouts) to be responsible and conservative, and rightly so. At the same time, the RBI governor was recently on record saying that the MPC is as a collective not even discussing rate cuts even though some members have individually hinted at that. One can argue that what went against the economy in FY24 – deflator being significantly lower than retail inflation – simply went the other way in FY23. But as noted, response has not been symmetric as rate increases have not been followed by cuts. There are of course global factors here as well.

This calls for statistical, definitional, and conceptual reforms in the conduct of India’s monetary policy.

First on the statistical side, the base year (2011-12) needs to be updated urgently – a richer India will have different consumption weights (as Engel’s law suggests, whereby staples reduce as a fraction of the basket as incomes rise) and there needs to be more accurate reflection of subsidised prices for food and other items (else fiscal-monetary coordination gets impacted.)

Second on the definitional side, the inflation target must be kept at the same numerical range but should be evolved to incorporate producer prices as well so that the differential with the deflator is removed or at least significantly reduced, otherwise retail inflation especially core will always remain on the higher side in our fast-growing economy as it is more services-dominated.

Third and finally on the conceptual side, RBI MPC needs to contemplate releasing our version of the US Fed’s Summary of Economic Projections (SEP, including “dot plots”) which would reveal a more official and current view of the central bank on the real neutral rates as well as sustainable growth and unemployment rates. “Normal” growth, inflation and employment estimates - though elusive - help to anchor monetary policy. So if we are now at low deflator and normal employment, say, then why is effective short-term risk-free at almost 7% when it should be much lower (more on this briefly below).

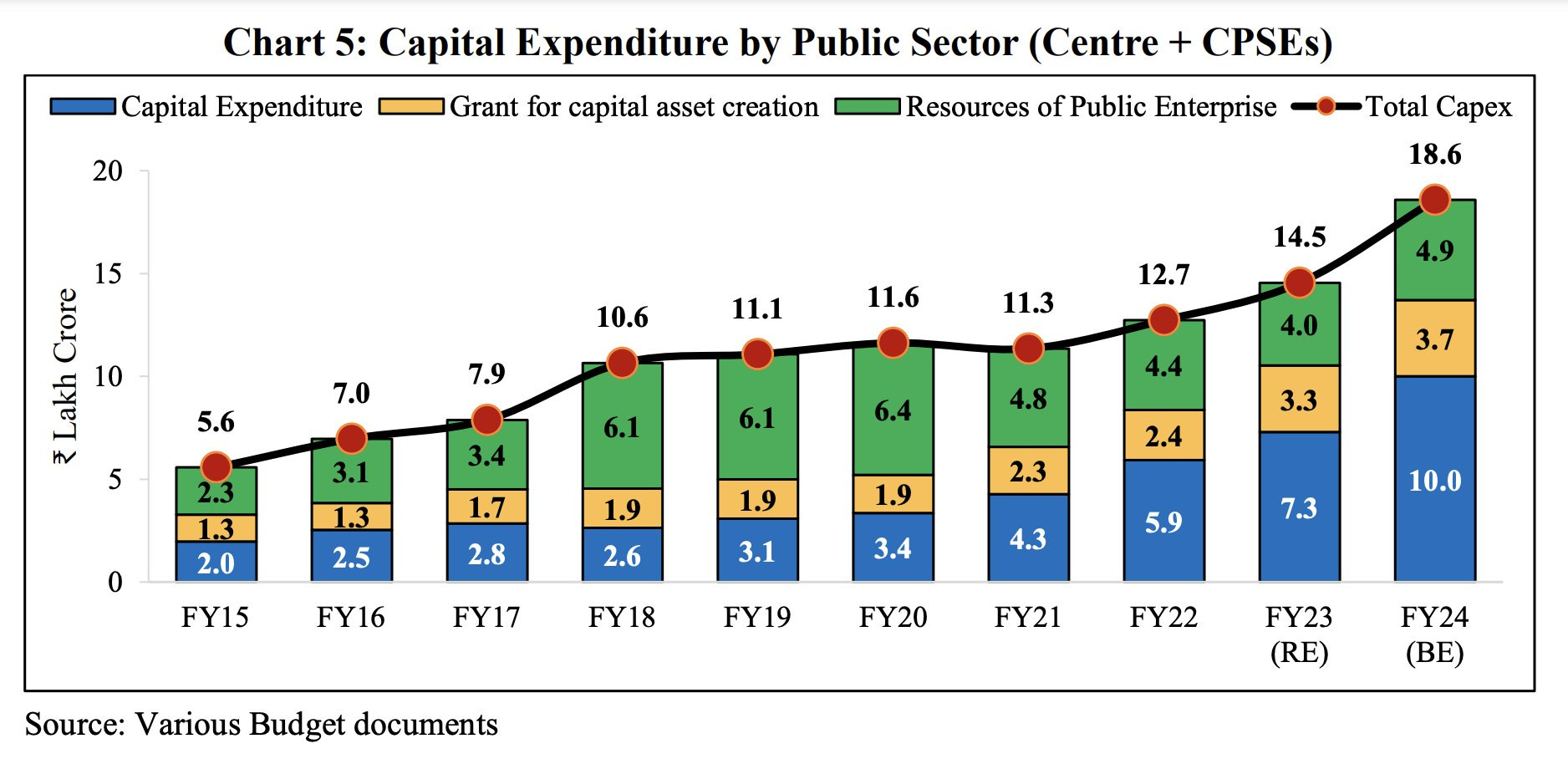

Why is this particularly important at this junction of our political economy history? The Modi government and Sitharaman Finance Ministry have, on a relative basis, not gone on extravagant fiscal expansion during and after the pandemic. Instead, they have dramatically increased capital expenditure (see: graph below) while putting in place a more efficient and pragmatic safety net for the larger population. In combination with earlier corporate tax cuts and a more proactive industrial policy, this is a dramatic supply side boost.

However, the demand side has been somewhat lagging – especially on the lower end – though better data is needed to corroborate this. Demand side can get a monetary policy boost but equally there is need for more significantly higher government spending in a few areas (which become both demand- and supply-side boosts).

Defense indigenisation and increased capex, industrial policy (such as the production-linked incentive schemes), a strategic and critical climate transition, more human capital and physical infrastructure investments all are likely to cost more money, even as general spending gets more efficient with time. These are all necessary investments.

And the only way to square the circle of gradual fiscal consolidation with similar tax rates (even keeping in mind some revenue buoyancy) is to reduce the gap between the fiscal and the primary deficits, that is, by reducing interest rates if macro-economic conditions so justify.

India’s demographic window is real (about a generation from here on) but it will likely be somewhat smaller than many projections given the dramatic transition in family sizes. We have no option but to invest more and invest soon. Given that the inflation-target regime was adopted in 2016, and despite the global inflation spike during the pandemic’s later phase, it is time to accept that in a broader and substantive sense we have done well with respect to inflation (once again, deflator over the last decade was around 4%.)

With the US having a SEP-median estimated inflation-adjusted neutral rate (r*) target of 0.5% even now (though the dispersion has increased towards the higher end) and India entering various global bond indices gradually beginning this year, it is difficult to argue for a r* of more than 1% for India (RBI also has a similar, although less official, estimate).

Longer-term natural rates differ from short-term neutral rates, finding them is often a complicated and imperfect statistical exercise, inflation rates vary as we saw depending on metrics, but still even with a 1% r* for India its neutral nominal short-term rate should be 5%. We are currently at 6.5% or higher even as our nominal growth rate is for now temporarily back to high single digits and labour force participation rates remain relatively low. Even if r* is slightly higher and the reality of following the Fed to some extent remains (even if unacknowledged), still policy is tight.

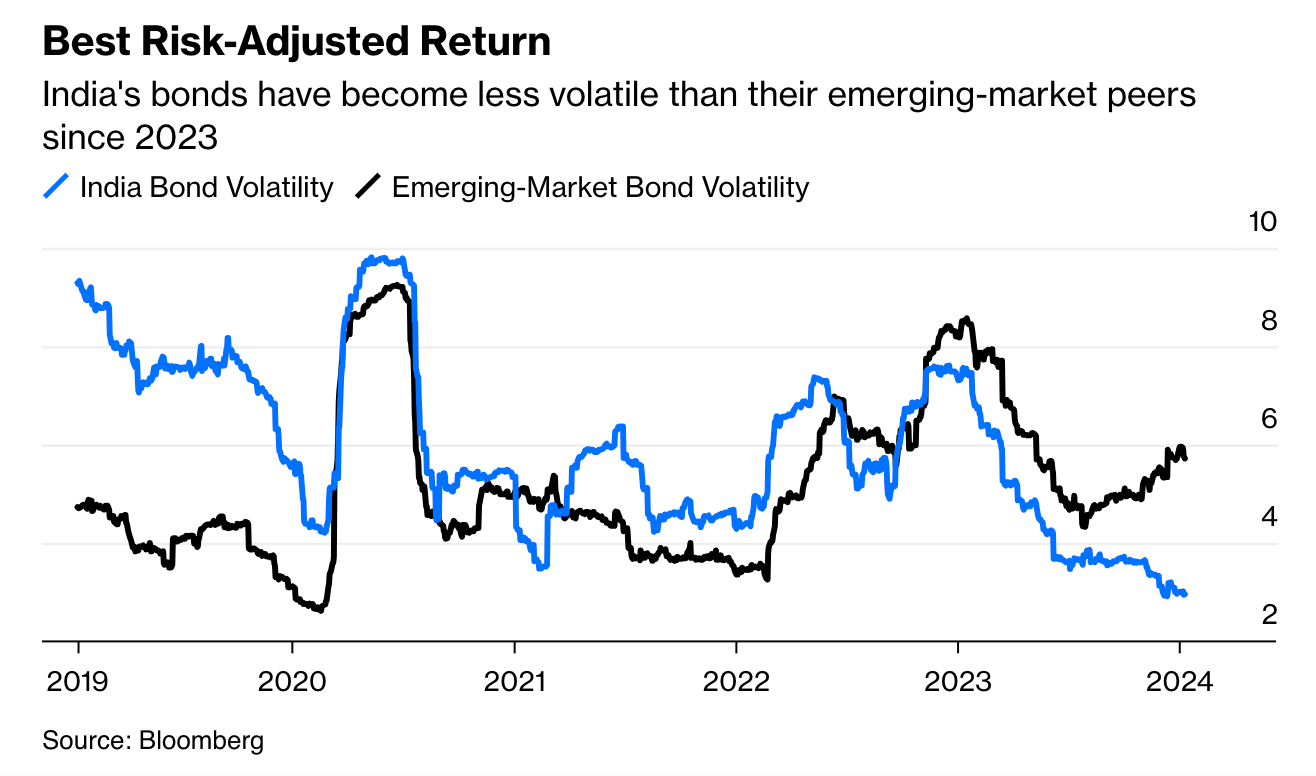

Without further monetary policy reforms, it would be difficult for India to leverage the Modi-Sitharaman reforms, infrastructure capital expenditure and remarkable fiscal management during a relatively tough period (and mostly irrespective of election cycles). The RBI also is one of India’s most critical and professionally run autonomous institutions and Mr. Das is globally recognised as one of the best central bankers. Indeed, the chart below on emerging market risk-adjusted bond returns shows our macro-institutional strength: India’s rupee and rates’ management in particular have been commendable in recent years.

But the RBI, particularly the MPC, needs to evolve its target and methodology to further deepen macroeconomic stability and growth - while not changing the 4% inflation target. Else we would simply leave significant money on the table (as the same chart above shows) for risk-averse domestic and foreign investors, without stimulating growth further in a sustainable manner. There are more loans for houses, education, companies, infrastructure and factories that need to be taken out for a much richer and fairer India. Sooner or later, this will adjust thanks to global bond inflows and India’s increasing scale, but if we manage this better we can reduce the formation of excesses.